Quantitative Transition Risk Assessment for Financial Institutions

Aligned with RBI's Disclosure Framework, TCFD, and NGFS scenarios, EnDecarb.ai provides the analytical engine to compute climate-adjusted financial risks.

The Regulatory & Strategic Pillars

Our framework aligns with global regulatory guidance and Reserve Bank of India expectations, addressing the key drivers of transition risk:

Policy & Regulatory Risk

Impact of carbon pricing, emissions trading systems (ETS), and evolving climate regulations.

Technological Disruption

Adoption of low-carbon technologies and risks from the phase-out of carbon-intensive assets.

Market Dynamics

Shifting consumer preferences and demand patterns affecting revenues and competitiveness.

Reputational & Strategic Risk

Changing investor expectations, ESG scrutiny, and implications for access to capital.

From Integrated Models to Financial Risk Intelligence

We employ a sophisticated six-stage downscaling methodology to translate global climate pathways into portfolio-level financial risk insights:

IAM & Transition Pathways

Integration of Integrated Assessment Models (IAMs) and global literature to project carbon pricing, policy shifts, and macroeconomic pathways across multiple climate scenarios and time horizons.

Asset-Level Overlay (Financed Emissions)

Mapping counterparty-level emissions (Scope 1, 2, and 3) against transition pathways to identify carbon-intensive and risk-exposed assets.

Transition Vulnerability Index (TVI)

Inhouse developed scoring framework assessing counterparties based on emissions intensity, sector exposure, and transition capacity under evolving policy, technology, and market conditions.

Model Ensembling & Calibration

Combining multiple scenario frameworks (NGFS, IEA, ECB) and calibrating them with India-specific macroeconomic variables, energy mix trajectories, and policy signals.

Financial Impact & Credit Risk Translation

Quantifying impacts on revenues, costs, and capital expenditure, and translating these into climate-adjusted probability of default (PD) and credit risk metrics.

Portfolio Aggregation & Transition Risk Database

Centralizing outputs into a unified database to enable portfolio-level insights, sectoral risk concentration analysis, and scenario-based stress testing.

Key Features of the Tool

Advanced Stress Testing & PD Modeling

Climate-Adjusted Financials

Generate projected balance sheets and P&Ls for corporates under multiple climate scenarios.

PD Stress Testing

Quantify how transition costs (energy mix shifts, carbon taxes) impact a counterparty's Probability of Default (PD).

Consistency across reports

Consistency across reports- Reduced manual effort

- Faster turnaround

Energy Mix Trajectories

Sector-specific modeling of energy consumption, renewable adoption, and brown-energy phase-outs.

Macro-Variable Pathing

Integrated pathways for inflation, interest rates, and commodity prices influenced by climate shifts.

Global Applicability

While grounded in ECB's economy-wide methodology, our tool is fully customized for Indian and global markets using all NGFS scenarios.

Portfolio Risk Intelligence

Gain a comprehensive, portfolio-level view of transition risk with decision-ready insights across sectors, geographies, and scenarios:

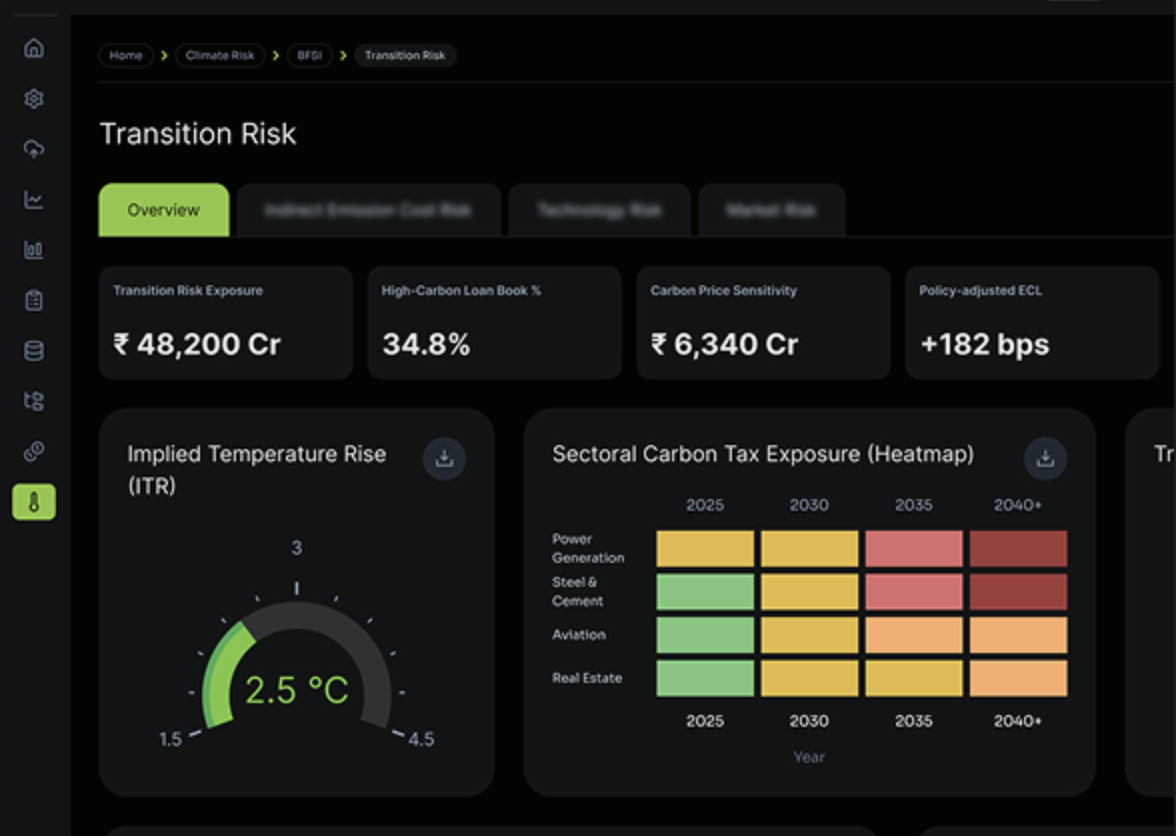

Sectoral Heatmaps

Identify high-risk exposures across sectors such as cement, steel, and power, with clear visibility into concentration and vulnerability.

Scenario Comparison

Analyze portfolio performance under multiple climate pathways, including Orderly, Disorderly, and Hot House World scenarios, across different time horizons.

Climate-Adjusted Risk Metrics

Track changes in probability of default (PD), credit risk, and exposure at risk under each scenario.

Country & Sector Aggregation

View risk distribution across geographies and industries to identify concentration risks and diversification opportunities.

Drill-Down Analytics

Navigate from portfolio-level insights to sector, counterparty, and asset-level risk drivers.